Daily market outlook 06.06.24

Macro Data

Today, Thursday, June 6, we have a couple of important macro data points coming up. First, we get the ECB rate decision at 8:15 am EST, followed by the weekly US jobless claims and unit labor cost at 8:30 am EST. The ECB press conference with Lagarde is then 15 minutes later.

ECB Day:

The overwhelming consensus is for a 25bp cut today, reducing the main refinance rate from 4.5% to 4.25%. Based on various ECB board member speeches over the last couple of weeks, this seems like a fixed outcome already, so don’t expect much more than a couple of pips on the € to the downside across the board. We should then see the classic “fade before presser” move, but be careful with the US data in between interfering—you may want to stay away from the EUR/USD on that trade and focus on a € cross pair.

All eyes will then be on the press conference to get any hints on future cuts down the line. Are we going to see a couple of consecutive 25bp cuts into the year-end, or are they going to hold for one or two meetings now? Only time will tell. In my opinion, though, chances are high that we see a little shift from Lagarde, trying to stay hawkish to a more moderate stance on things as we edge closer to the first FED cut as well, with the ECB just trying to mirror the big brother as much as possible. I would not be surprised to see the market taking the shift from Lagarde as a minor dovish one, but I’m still open to the idea that the ECB still wants to drag this out for as long as possible.

Let’s check the data over the last couple of months.

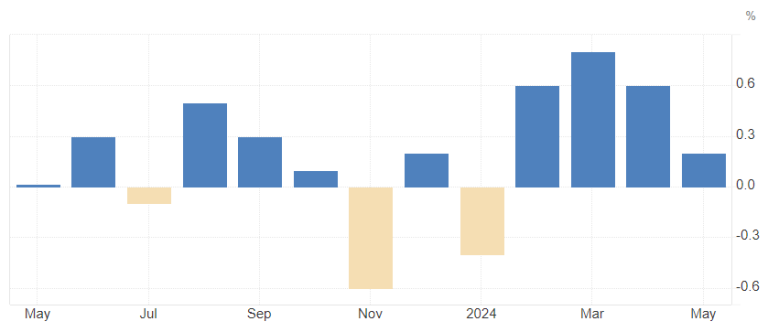

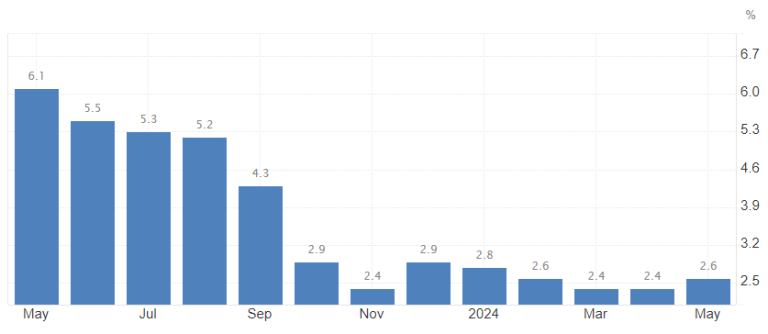

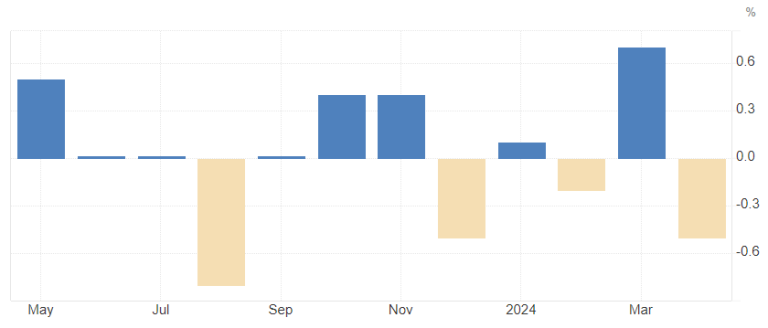

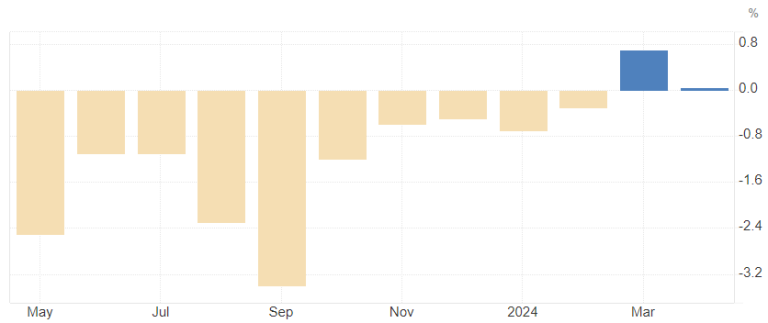

Euro Area headline inflation MoM experienced the same spike at the beginning of the year as the US and basically everywhere else in the world, but since then has calmed down quite a bit again, with the latest report coming in at 0.2% for May. That in turn translated to a YoY reading of 2.6%—and we have been really steady on that one between roughly 2.5 and 3% since October 2023 already.

EU MoM headline Inflation

EU YoY headline Inflation

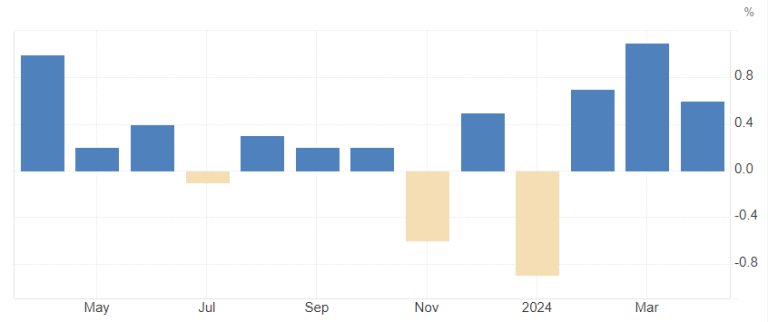

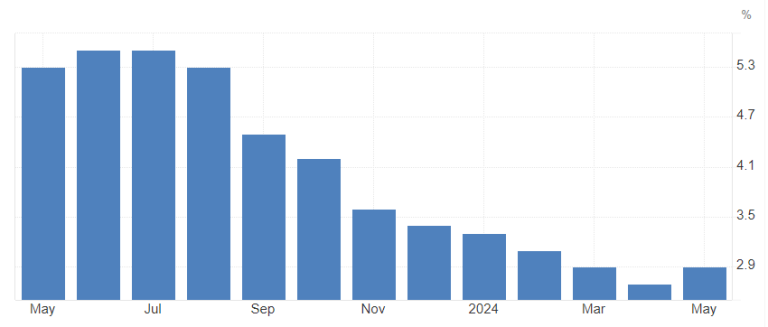

Core inflation is on the same path. We did not yet get the May data, but April came in at 0.6% MoM compared to the same reading on the headline for April. YoY we see a well-declining chart, maybe bottoming out a bit between 2.5 and 3% as well now going forward.

EU MoM core Inflation

EU YoY core Inflation

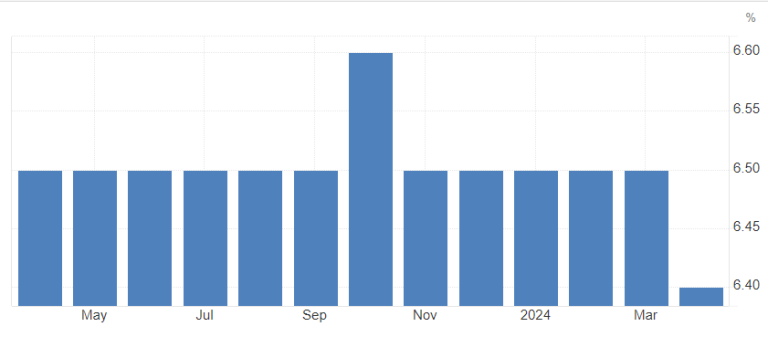

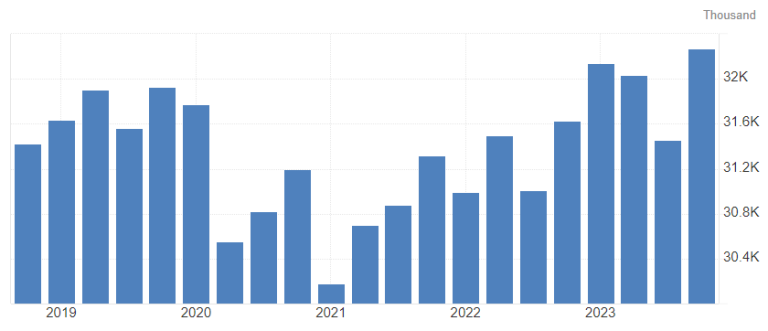

Unemployment in the Euro Area is steady around 6.5% so far, with no real sign of any changes there yet. An interesting but mostly overlooked fact is the move from full-time employment to part-time employment, with the latter clearly on the rise since the bigger COVID dip.

EU unemployment rate

EU part-time employment

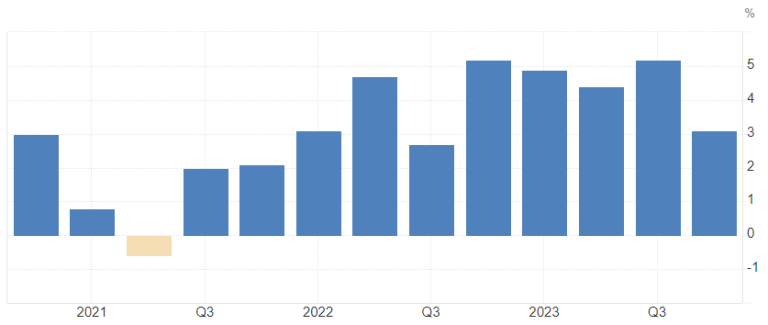

Wages are something the ECB really leaned into for a reason to keep rates high, but they are so lagging that it just does not make sense to use it as a gauge for “should-be” forward-looking monetary policy changes. That said, annualized Q4 wage data was coming down massively from around 5% in the quarters before it, to 3.1%.

EU wage growth QoQ

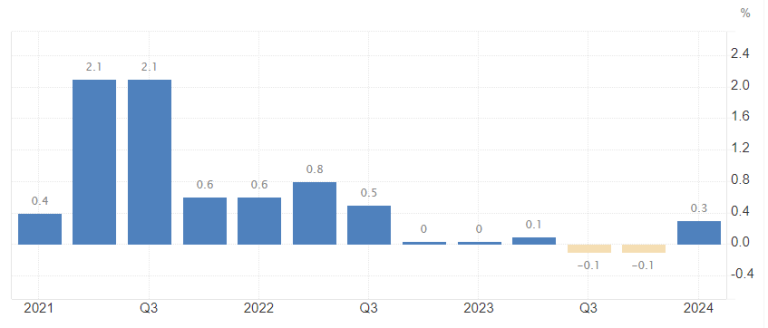

GDP growth is pretty much flat: 0.3% in Q1 2024 after two consecutive quarters of 0.1% contraction.

GDP growth QoQ

Retail sales are sluggish as well and consolidating around 0% now

EU retail sales MoM

EU retail sales YoY

Based on the data, it is okay to say that the ECB is already late in the cutting cycle (especially compared to other central banks), and it would not be surprising—as mentioned above already—that we are in for consecutive cuts until the year end.

Jobless Claims and US Unit Labor Cost:

I’m not going to write up too much about that—as usual—be careful with those numbers, especially the unit labor cost, as that has been a bigger mover in the last couple of quarters. I’m not expecting huge moves on it like every week, though, especially with everyone focusing on the ECB.

Going to come up with an NFP-Outlook tomorrow!

Good luck, and as always—set your risk limits!

Dom

.png)

.png)

.png)