Macro data summary week 29.04.24 – 03.05.24

May 6th 2024

A big highlight for last week came early Monday Asia session already, with the USD/JPY climbing from 158 to 160 in a violent stop move, clearing 158.65 to 160.16 in a single minute. We rejected 160 in an expected move and settled around 159 for a good while. Roughly two and a half hours later, we saw enormous selling pressure kicking in, approximately 100 pips in a minute, followed by more selling pressure. In the end, we cleared more than 400 pips (159.4 to 155.25) in less than an hour, which certainly looked like a BoJ/MoF intervention. The rest of the day was volatile in an up-and-down trading, settling at 156 flat on the day.

The data front started up slowly on Monday with the German prelim CPI for April, which came in a tick softer than expectations on the headline and on-spot at the harmonized index.

Tuesday started up the week for real with the China NBS manufacturing (softer) and non-manufacturing PMI (stronger) as well as the Caixin manufacturing report (softer) in the morning, then continuing with EU prelim CPI for April which was ticking down both on Headline – 0.7% MoM vs 1.1% MoM last time – as well as on the harmonized index at 0.6% MoM vs 0.8% MoM last time.

EU prelim GDP for Q1 came out same time and saw a sweet upside surprise at 0.3% QoQ vs flat for Q4 2023 and 0.1% expected.

Tuesday finished off with the US employment cost index for Q1 which came in at 1.2% vs 1.0% expected and 0.9% last quarter, showing some surprisingly strong underlying wage pressure there, underlining the strong labor market data we saw during all of Q1.

Wednesday then being the first of May, meaning we had “Labour day” in most of Europe which is a banking holiday. New Zealand then reported their job data for Q1 which came in weaker than expected, with an upticking unemployment rate to 4.3% from 4.0% and 4.2% expected. Participation rate also fell down slightly from 71.9% to 71.5%. Labor cost index was down two ticks as well from 1.0% to 0.8% QoQ.

Later in the US session we got the ADP report which came in stronger than expectations at 192K vs 175K expected and 208K last time (revised from 184K) again showing the strong Labor market in the US.

We also got S&P global manufacturing on Wednesday for both Canada (49.4 vs 50.2 ex and 49.8 last) and the US (50 vs 49.9 ex and 49.9 last).

The data highlight of the day was the ISM manufacturing report at 10am EST. It came in pretty weak to surprise a lot of economists.

Headline 49.2 vs 50 expected vs 50.3 last

Employment 48.6 vs 47.4 last

New orders 49.1 vs 51.4 last

Prices paid 60.9 vs 55 expected vs 55.8 last

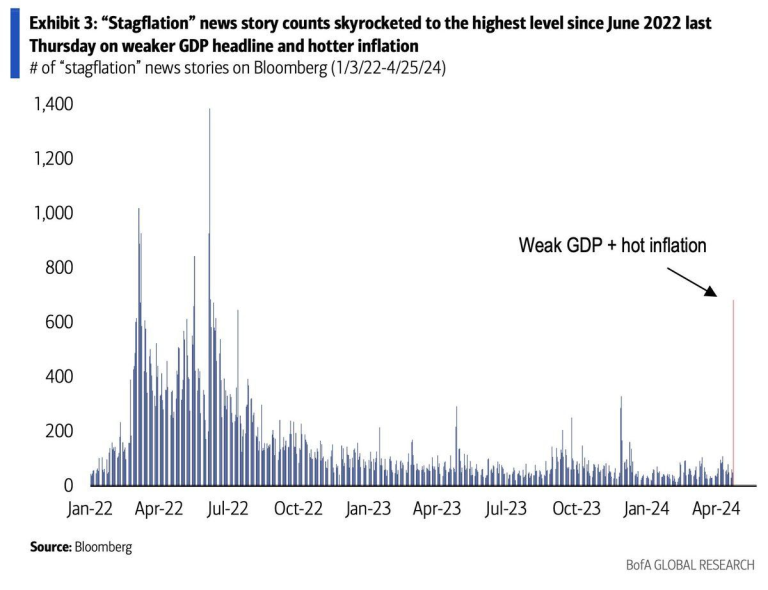

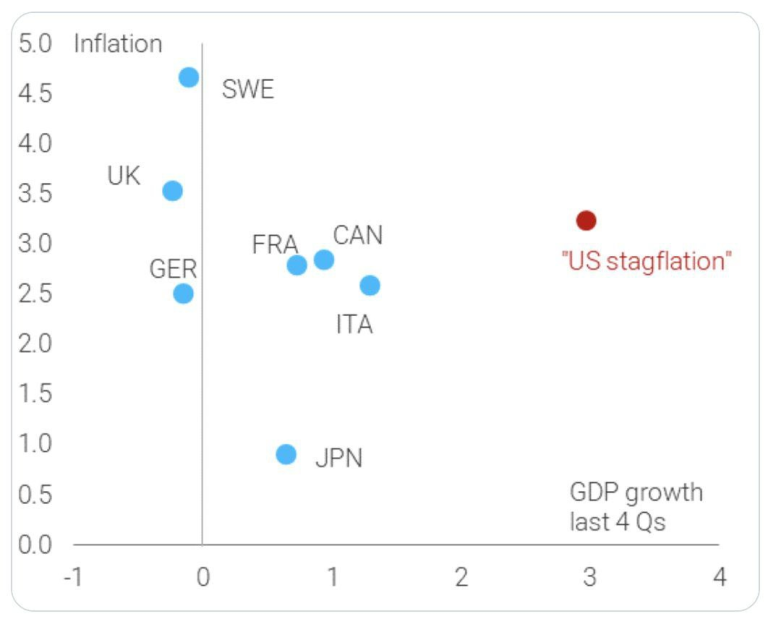

As you can see there, the prices paid sub-index was running super hot again with a reading above 60 – that really sparked some fears of higher inflation for longer, coupled with underlying growth and labor market weakness in the rest of the report, which in turn sparked some early fears of stagflation. On X, the word “Stagflation” started to slowly trend higher from Wednesday onwards, and only kept getting more trendy into the end of the week.

That wasn’t all though for the day, we still had FOMC on the docks.

The FED held rates as expected at 5.5%. The real deal was the press conference 30min afterwards. Pretty much EVERY journalist tried to bait FED chair Powell to give a hawkish comment, trying to get him to say something along the lines of “we possibly need another hike” or “we are not sure that current rates are restrictive enough”, but no, Powell stand the ultra-dove and delivered a wall against those bait-questions. He reassured that data is something they are monitoring, but it is not yet too strong and they are not thinking about hikes at this point. The doves found their messiah during that first roughly 40mins of press conference. We have to understand that market pricing was extremely hawkish into the FOMC meeting with expectations being for a overly-hawk Powell. He didn’t deliver.

Same time, he was not too dovish either, stating that the road is going to be bumpy, and a little weakness in the labor market wouldn’t be enough to get them going on the rate cut path. That really turned around the dovish sentiment on the 2nd thought about the presser – YES, it was less hawkish than expected, but NO it was not dovish. Markets essentially faded the dovish moves all across the board at the end of the presser.

The day ended with the highlight of the day; another BoJ / MoF intervention on USD/JPY, trading at 157.5 at the time and rising back from the dovish FOMC move earlier (low at 157 flat). Price really plumetted clearing 154 roughly 30min after it started. It then looked like price was going to settle there, however we found ourselves bouncing up to 154.8 before getting hammered down to 154 flat again, where we settled for a couple of minutes. As this was just half a hour before rollover, we had ultra-thin liquidity in the market. In the end we had another dip lower to 153 flat before it bounced like a “man on fire” into the rollover up to 154.5 again. Extremely volatile trading on USD/JPY all week long.

Thursday then saw us having Swiss CPI coming in a bit hotter than expected at 0.3% MoM vs 01% expected and 0.0% last. US weekly jobless claims been up as usual too, coming in hot still at 208K vs 212K expected and 208K last week (revision from 207K). Unit Labor Cost was released the same time for Q1 and saw it flying to 4.7% vs 3.2% expected and 0.0% last quarter.

Friday then finished off the busy week with NFP and ISM services on the dock. Non-Farm-Payrolls was simply weak across the board, from headline at 175K vs 243K expected and 315K last month (revised from 303K), to the unemployment rate at 3.9% vs 3.8% expected and last, up to the average hourly earnings at 0.2% MoM vs 0.3% MoM expected and last. Even weekly hours ticked down to 34.3 vs 34.4 last and expected, U6 underemployment also ticked up to 7.4% vs 7.3% last. In the end there was no reading that showed anything promising for the hawks. S&P global services and composite was then released in between the NFP and ISM report, coming in at 51.3 for both, vs 50.9 expected and last time for both as well – a welcomed surprise.

ISM services was then exactly the same as the manufacturing report on Wednesday:

Headline 49.4 vs 52 expected vs 51.4 last

Employment 45.9 vs 48.5 last

New orders 52.2 vs 54.4 last

Prices paid 59.2 vs 53.4 last

This, coupled with the soft NFP report, really sparked lots and lots of talk about stagflation and it was super trendy on Friday on X.

.png)

.png)

.png)