a recap of events last week

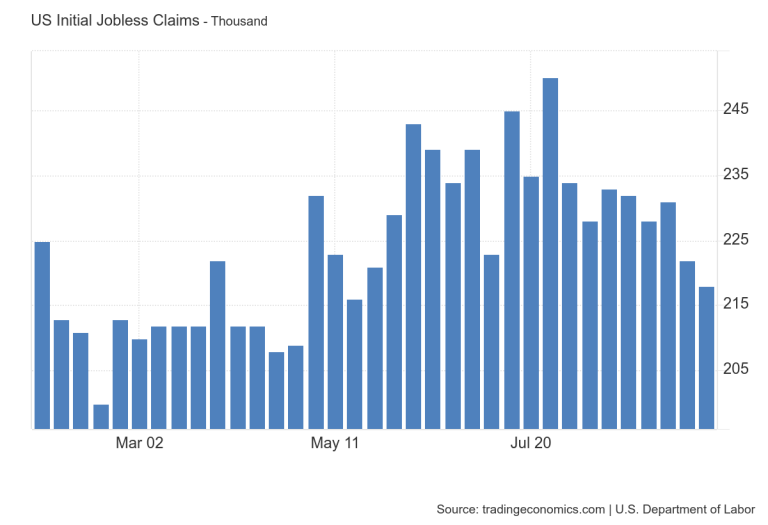

Last week, several key economic indicators were released that provided insights into the U.S. economy’s current health and trajectory. U.S. initial jobless claims for the week were reported at 218,000, coming in lower than forecasts of 223,000, signaling continued resilience in the labor market. However, continuing claims, which reflect the number of individuals still receiving unemployment benefits, rose to 1.834 million, suggesting that while new claims are falling, re-employment may be slowing.

In a positive development, durable goods orders surged by 3.5% month-over-month in August, significantly above economists’ expectations of a 2% increase. This reflects robust demand in key sectors such as transportation and machinery, indicating possible strength in future manufacturing activity. The previously anticipated downward revision of second-quarter GDP growth from 3.0% to 2.9% was notably absent, with the economy maintaining its growth momentum, buoyed by stronger consumer spending and business investment.

In the financial markets, expectations for year-end Federal Reserve interest rates edged higher by a few basis points following recent economic releases, despite the U.S. dollar experiencing renewed selling pressure after some position adjustments on Wednesday. Market participants are still pricing in a 50 basis point rate cut at one of the upcoming Fed meetings, as traders weigh the potential impacts of economic data on monetary policy decisions.

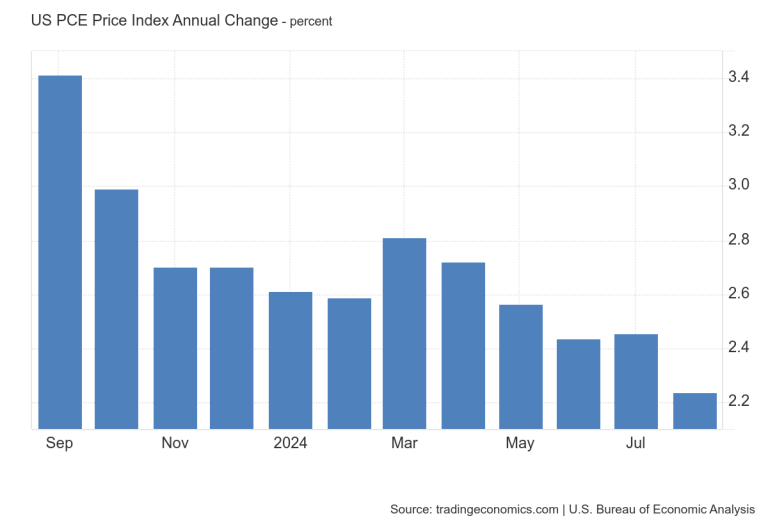

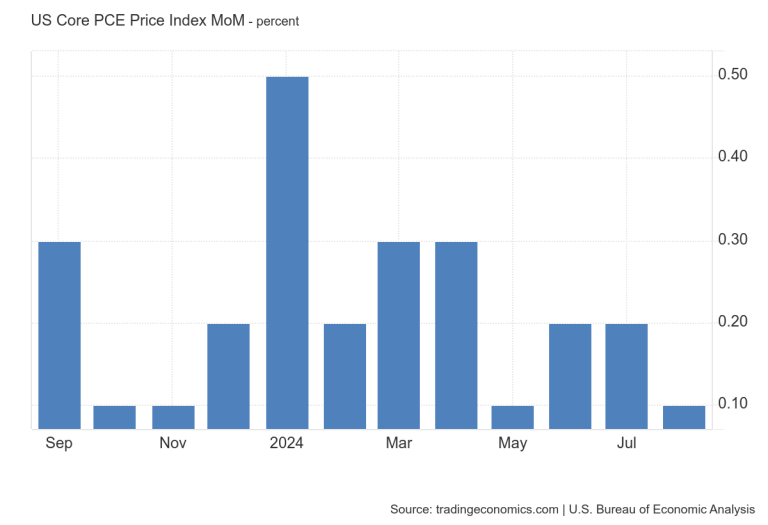

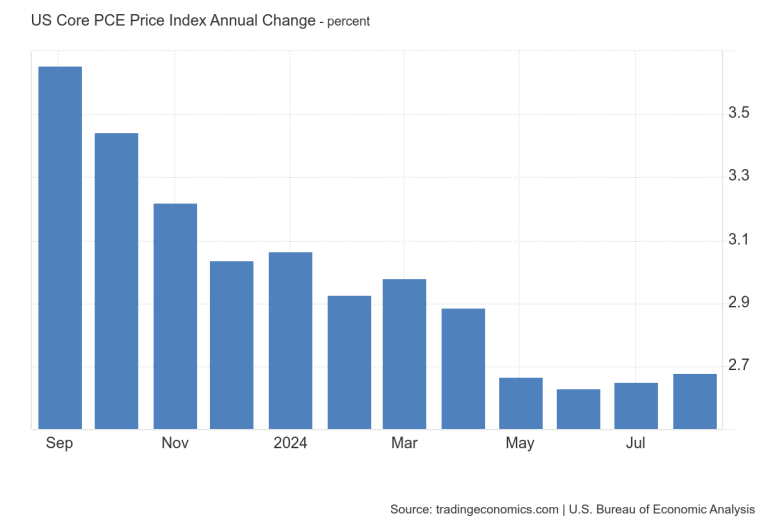

Inflation data released by the U.S. Bureau of Economic Analysis (BEA) on Friday showed that the headline Personal Consumption Expenditures (PCE) Price Index rose by 2.2% year-over-year in August, slightly lower than the market consensus of 2.3%. In terms of monthly changes, the PCE Price Index increased by 0.1%, aligning with analyst projections. The core PCE Price Index, which excludes the more volatile food and energy segments, also rose by 2.7% on a year-over-year basis, matching market expectations. However, the monthly growth for the core PCE was just 0.1%, below forecasts, suggesting that inflationary pressures may be losing steam.

Additionally, consumer confidence, as measured by the Conference Board Index, increased to 133.5 in August, up from a revised 127.9 in July, indicating improved optimism among consumers about current business and employment conditions, which may support consumer spending moving forward.

Overall, these data releases suggest that while the U.S. economy shows signs of strength, particularly in manufacturing and consumer sentiment, underlying challenges such as rising continuing claims and softer inflation readings could influence ongoing monetary policy discussions within the Federal Reserve.

.png)

.png)

.png)