horizon trading edge

Market Blog

Horizon Trading Market Blog

Weekly market outlook for 06.05.24 – 10.05.24

May 6, 2024

Monday kicked off with April HCOB PMIs for Europe, which came in slightly higher on average.

Spanish services 56.2 vs 56 ex vs 56.1 last

Italian services 54.3 vs 54.7 ex vs 54.6 last

French composite 50.5 vs 49.9 ex vs 49.9 last

French services 51.3 vs 50.5 ex vs 50.5 last

German composite 50.6 vs 50.5 ex vs 50.5 last

German services 53.2 vs 53.3 ex vs 53.3 last

EU composite 51.7 vs 51.4 ex vs 51.4 last

EU services 53.3 vs 52.9 ex vs 52.9 last

That was not really a market mover today.

We also got EU PPI today already which came in at -0.4% MoM, beating expectations of -0.7% and “up” from last time of -1.1% (revised lower from -1.0%).

Overall, some slight uptick in euro data there, but PMIs still around 50 and PPI still negative.

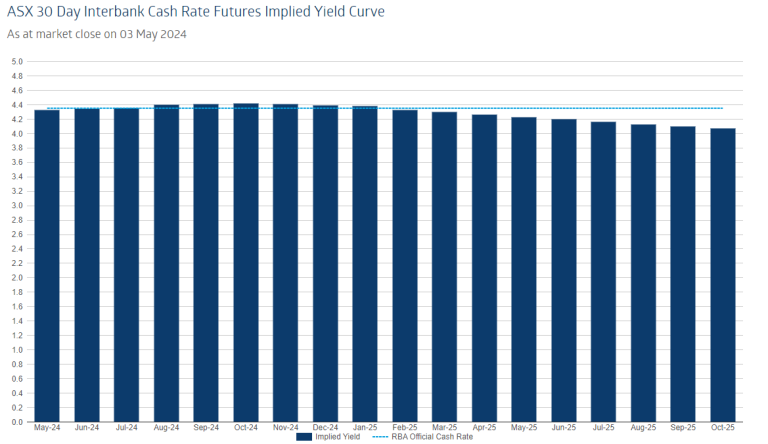

Further on the docket, we get the RBA interest rate decision in Tuesday’s Asia trading, followed by the press conference 1h after.

Expectations are for a “hold” at 4.35%, and that’s my base case as well.

Eyes are going to be on RBA Governor Michele Bullock whether she’s seeing the need for further rate hikes before the end of the year.

Implied market data shows an expected peak at 4.415% in October, which is not enough for another 25 hike. End of the year shows rates at 4.39%, and the first cut only by August 2025 with an implied rate of 4.125%.

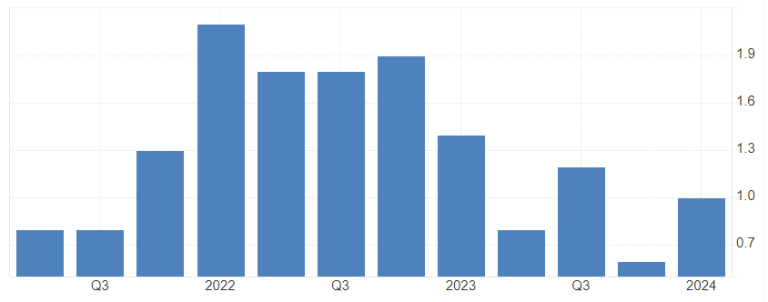

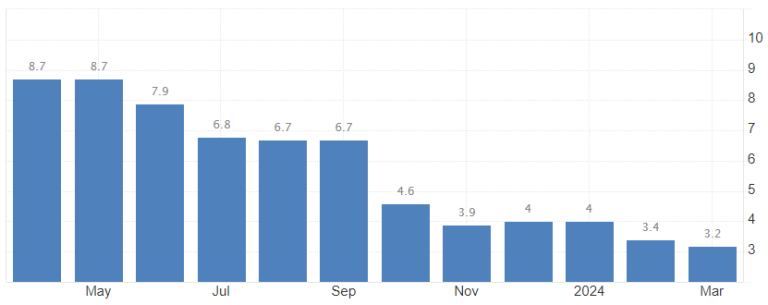

Recent Australian inflation data came in at 0.6% for Q4 2023 and 1.0% for Q1 2024. YoY inflation dropped from 4.1% in Q4 to 3.6% in Q1, respectively. Trimmed mean CPI is still ranging higher from 0.8% in Q4 to 1.0% in Q1 as well.

AU YoY headline CPI

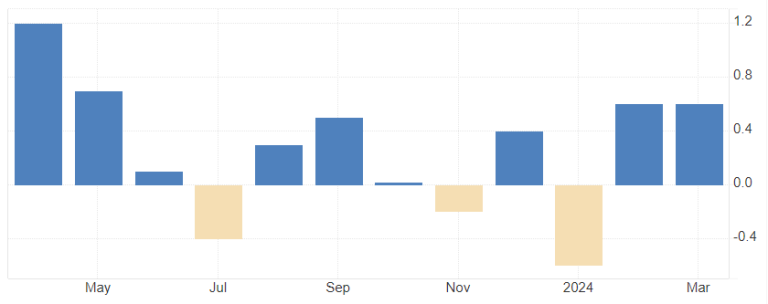

AU QoQ headline CPI

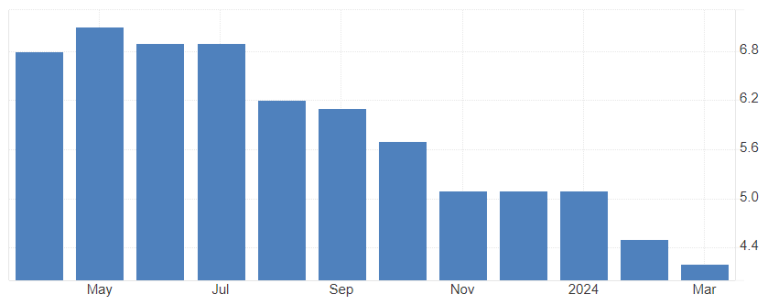

AU YoY trimmed mean CPI

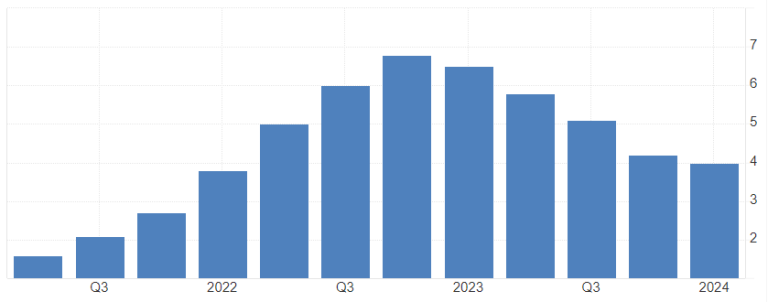

The labor market in Australia is pretty volatile lately but still steady and not showing any signs of abnormal easing or further tightening just yet.

All of that combined leaves some question of further hikes needed – I don’t think so honestly, and we see some underlying weakness in retail sales throughout the year so far, which could indicate that higher rates are slowly but steadily creeping into spending, leading to slowing inflation further down the road.

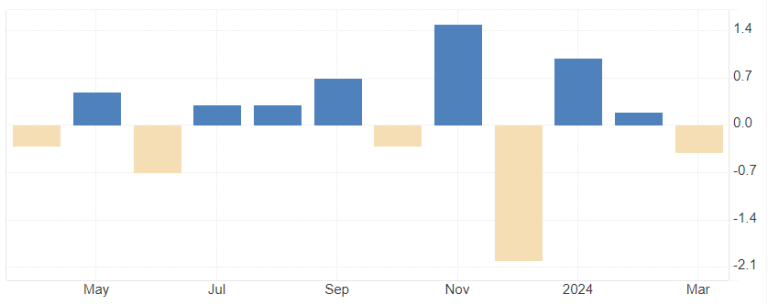

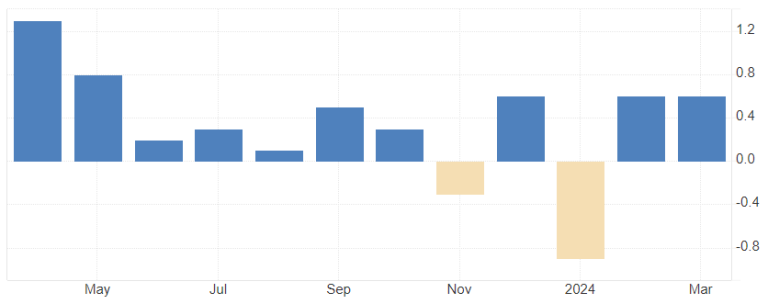

AU MoM retail sales

I don’t think it’s yet time for rate cuts, and the market is acknowledging that as well. However, I too think the market is too bullish on the inflation path, with quarterly numbers quickly falling to 0.8% on average for the rest of 2024 then accumulating to 3.44% for 2024 and falling to 0.5% quarterly on average for 2025, which would accumulate to exactly 2.01% for next year.

So with that projection in mind on my side, I see the rate path too bullish and expect a shift to the dovish side a bit later in the year when more data is available – especially eyeing the Q2 inflation and jobs data that should show early weakness.

Looking at the AUDUSD, we are trading at 0.662 for the time being, right at the upper range of the 2024 trading range, which is also home to the 50% level of the December 2023 high to April 2024 low move, coming in at 0.6617.

Last week saw us trading higher, clearing and settling above the 100-day SMA currently located at 0.658.

I think a relatively neutral Bullock should let us test some further upside, maybe going to and clearing the March highs at 0.6667 before fading and turning down again towards the 100-day SMA.

I don’t think this RBA meeting is going to be THE big mover on the AUD, barring any surprises on both sides.

Rest of Tuesday is relatively quiet, only getting EU retail sales in European trading, Canadian IVEY PMI report at the 10 a.m. EST dock, and a 3-year US bond auction at the usual 1 p.m. EST. All of those aren’t expected to be big moves, but keep an eye on the IVEY for small CAD moves and the 3-year auction barring any surprises.

Wednesday then completely empty except for some Fed speakers and a US 10-year auction + Ascension Day in Germany, France, and Switzerland (banking holiday).

Thursday is kicking off with China trade data in the middle of Asia trading, then going further with BoE day.

Expectations are for a “hold” in the UK as well at 5.25% with close to a 100% chance.

Thus, all surprises are going to hide in the press conference that is coming up 30 minutes after the rate decision.

BoE Governor Andrew Bailey is going to answer the journalists’ questions, and I think he could deliver a pretty dovish move there, indicating that the path of inflation in the UK is sufficiently down, leaving the door open for a rate cut as soon as the next meeting on June 20th.

In fact, in their last report from February, the BoE forecasted that the bank rate will fall towards 5.1% in Q1 2024 and to 3.9% for Q1 2025, with a median rate of 4.2% through 2024, based on implied overnight index swap rates.

heres is a link to their website

That also assumed that YoY inflation shortly dips below 2% in spring before bouncing again into the middle of the year towards 2.5 to 3.0%.

The recent CPI after the February meeting then came in at 0.6% MoM for both February and March, with YoY readings falling from 4.0% in January to 3.4% in February and 3.2% in March.

UK YoY headline CPI

UK MoM headline CPI

Core inflation MoM saw 0.6% increases for both February and March too, with the YoY readings coming in at 5.1% in January, 4.5% for February, and 4.2% for March.

UK YoY core CPI

UK MoM core CPI

I certainly expect a dovish move on the GBP following a dovish Bailey press conference, really emphasizing a June cut and then more into the year-end, still saying they need to stay data-dependent. Looking at cable, we see the current rate is holding around the 1.255 mark, which is home to the 200 daily SMA, and up to 1.26 marking the bottom of the early 2024 range.

The 100 daily SMA currently sitting at 1.264 should provide resistance in case of a run higher, which is also home to last week’s/Friday’s high at 1.2635.

In case of a dovish move, I expect the pair to fall towards 1.2465, which marks the 50% level of the October 2023 low to March 2024 high. Barring any big USD or GBP news before the BoE meeting, it could very well be we are still trading around 1.255-1.26 into the meeting.

US weekly jobless claims will finish off the rest of Thursday, along with a 30-year US bond auction and some more Fed speeches.

Friday will see UK GDP preliminary data for Q1 in the morning, alongside a full slate of minor UK production and trade data at the same time. Canadian employment data and the Michigan Consumer Sentiment Index will finish off the week, along with even more Fed speeches.

All in all, the week is really quiet on the macro data side, besides the RBA and BoE meetings. Especially on the USD side, it’s very quiet, which means we’ll probably see more repercussions from last week, namely the “sort-of-dovish” Fed meeting and the really weak NFP report, along with the weaker-than-expected ISM reports, but strong Prices Paid sub-indexes.

Possible movers are the bond auctions, but as always, only if they are surprising in either direction.

Bonds will generally be something to watch. I think we could see a fade of the bounce in still-bearish sentiment and consistent fears of re-acceleration of US inflation with the aforementioned high Prices Paid readings. Since we don’t get the April inflation data until May 15th, we have to wait to see if that is falling along with growth data, or if it is really withstanding gravity and holding up high for whatever reason.

Don’t expect this week to be a huge mover all around, but I think the USD can bounce back a bit, going from 105.1 on DXY as of the time of writing, towards 105.5, which marked the breakdown level from last week, and maybe even getting back into the trading range towards 106 flat. On the downside, we have support coming in at 104.55 as the NFP low but a zone going up till 104.7 that should provide sufficient buying pressure in case we go down there. The weekly pivot comes in at 105.36 and the weekly R1 at 106.2. I doubt we’ll reach the S1, but just in case, it’s coming in at 104.23.

In equities, I think we are going to explore some more upside and test the yearly highs which are coming in at 5,265 for SPX, 18,700 on NQ, and 39,900 on DJI. These highs should be cleared in my opinion, before we see some settling into the weekend right around there.

Gold should hold the current range between $2,300 and $2,350 for the week, barring any huge surprises on the geopolitical level.

I expect some oil bounce, as we reached the 100-day SMA on the CL futures at $77.98 on Friday and today morning. Upside targets should come in at $80 – the weekly pivot as well as the 23% Fibonacci retracement level of the latest dip are there. $82.75 is home to the 50% level and a topside structure cluster, which should provide some further resistance up to the $83 level.

In case of a further breakdown, the next real support comes in at roughly $76, which is home to a bigger breakout level from December 2023 as well as the weekly S1. Further down, we have to eye S2 at $74 and the February lows at $71.5.

Another commodity I’m really looking forward to is cocoa. After the HUGE breakdown last week, I only see more downside this week.

First, we should retest the $7,000 level on the CC futures before we could see a potential move towards $6,666, which marked a breakout level in March this year.

I don’t think we are going to go massively lower than that – it would already mark an astonishing 43% drop in prices since the all-time highs on April 19th, so I will definitely cash out most of my puts at the $7,000 level and all at the $6,666 target.

I hope this outlook for the week provides some good insights and a decent preparation for the week – as always, take care out there and don’t risk too much!

Leave a comment of what you think could be a huge mover or THE thing to watch this week. Enjoy! – Dom

horizon market edge

.png)

.png)

.png)

©2025 Horizon Market Edge .